Choosing between fixed and variable mortgage rates in Canada has become one of the most important financial decisions for homeowners in 2026. With interest rates fluctuating and housing affordability under pressure, understanding how each option works is critical for long-term financial stability.

Understanding the current mortgage landscape in Canada is essential. Canada’s housing market has undergone significant changes in recent years. Rising home prices combined with higher interest rates have made mortgage decisions more complex than ever before. Despite rising interest rates, nearly half of Canadian borrowers are still choosing variable rate mortgages — a trend that reflects growing expectations of future rate cuts.

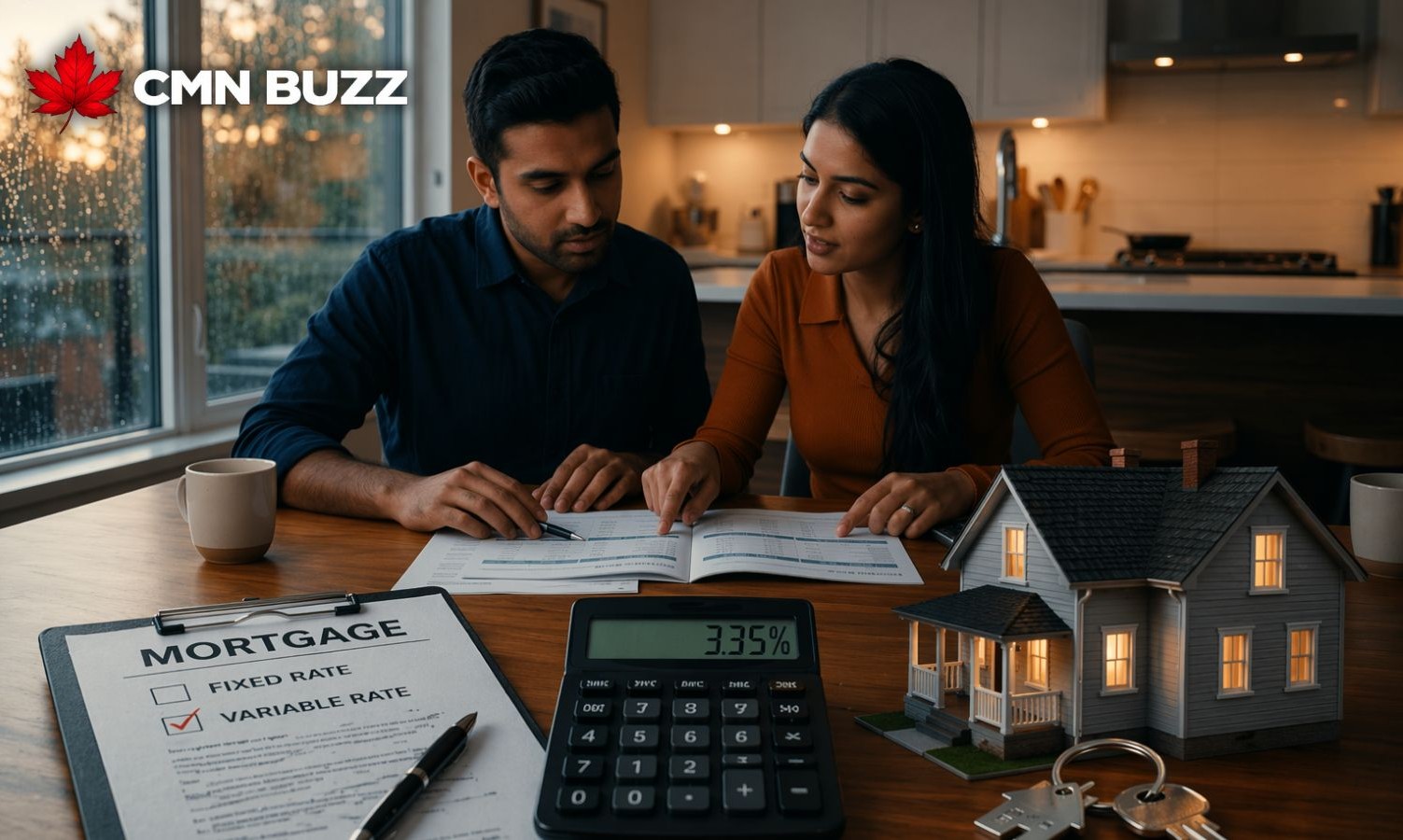

A variable rate mortgage is directly tied to the Bank of Canada’s policy interest rate. This means your interest rate can increase or decrease over time, depending on market conditions. As a result, monthly payments may fluctuate, borrowers may benefit if interest rates decline, and initial rates are often lower than fixed mortgages. For many homeowners, the lower starting rate makes this option attractive in the short term.

A fixed rate mortgage offers consistency and predictability. With this option, your interest rate remains unchanged throughout the term, monthly payments stay stable, and you are protected from market fluctuations. Although fixed rates are typically higher at the beginning, they provide financial security and peace of mind.

Several factors are influencing why Canadians are choosing variable rates. Variable rates are generally lower than fixed rates, making monthly payments more affordable in the short term. Many borrowers believe interest rates may decrease in the coming years, which could reduce their payments over time. In a high-cost housing environment, some homeowners prioritize immediate affordability over long-term stability.

While variable mortgages can offer short-term savings, they come with important risks. Monthly payments can increase if interest rates rise, budgeting becomes more difficult due to uncertainty, and financial stress may increase during rate hikes. Borrowers need to be prepared for fluctuations before choosing this option.

A large number of Canadian homeowners are expected to renew their mortgages between 2025 and 2026. This period is significant because many borrowers will face higher interest rates at renewal, monthly payments could increase substantially, and financial planning will become more important than ever. Even homeowners who previously locked in lower fixed rates may experience payment increases.

The right choice between fixed and variable depends on your financial situation and risk tolerance. Variable mortgages may work for those who can manage fluctuating payments, expect interest rates to decline, and want lower initial costs. Fixed mortgages may be better for those who prefer predictable monthly payments, have a tight budget, and want protection from future rate increases.

For newcomers to Canada, mortgage decisions can have long-term financial consequences. Without strong financial backing or family support, managing fluctuating payments may be more challenging. In such cases, stability and predictability often become more important than short-term savings. Careful planning and understanding the risks can help avoid financial stress in the future.

The increasing preference for variable mortgages reflects a broader shift in how Canadians are approaching financial decisions. There is a greater focus on short-term affordability, an increased willingness to take on financial risk, and changing expectations about future interest rates. This trend could shape the housing market for years to come.

The decision between fixed and variable mortgages is no longer just about interest rates — it is about risk, timing, and financial strategy. Is it better to save money today, or protect your financial future from uncertainty?

Key Takeaways

- Nearly half of Canadian borrowers are choosing variable rate mortgages despite rising interest rates

- Variable rates offer lower initial payments but come with higher financial risk

- Fixed mortgages provide stability but are currently more expensive

- Many homeowners may face higher payments during mortgage renewals in 2025–2026

- Choosing between fixed and variable depends on risk tolerance and financial planning

- Newcomers should prioritize stability if managing uncertain income

For a Malayalam news perspective on this topic, read the full report here.

Share your thoughts and questions about this news in the comment box below. For more information, visit our website or email us at cmnbuzzcanada@gmail.com. Follow CMN Buzz on social media to stay updated with all major news from Canada in real-time.

Stay tuned to CMN Buzz — Your trusted partner for news that shapes the future of immigrant life in Canada